01 Oct Bonita Bay Real Estate News | October 2023

As of October 1, 2023, there are 45 active listings in our area multiple listing service (MLS) in Bonita Bay; 6 more than last month.

For comparison, last year on Oct. 1, there were 23 listings in Bonita Bay.

There are 10 single-family homes on the market from $849,000 to $6,995,000. The average list price is $3,225,800 and the average days on the market is 140. The combined days on the market is 197.

There are 16 listings in the carriage, mid-rise, townhouse, and attached villa market with prices ranging from $449,900 to $985,000. The average list price is $677,219 and the average days on the market is 72. The combined days on the market is 91.

In the high-rise market, there are 19 active listings in Bonita Bay ranging in price from $1,290,000 to $5,450,000. The average list price is $2,976,579 and the average days on the market is 180. The combined days on the market is 207.

Your Bonita Bay REALTOR®,

Ed Gongola

SUMMARY OF BONITA BAY HOME SALES

If you are considering selling your Bonita Bay home, here are some statistics that may help you decide to place your home on the market:

BONITA BAY CARRIAGE, MID-RISE, TOWNHOUSE AND ATTACHED VILLA HOMES

- Within the last 12 months, there were 57 sales with an average sales price of $700,007; these condos were on the market an average of 32 days; combined days on the market is 80.

- During the 12 months previous, there were 93 sales with an average sales price of condominiums was $606,648; these homes were on the market for 11 days; combined days on the market is 52.

BONITA BAY HIGH-RISES

- During the last 12 months, there were 63 sales with an average sales price of $3,218,302; these homes were on the market an average of 124; combined days on the market is 439.

- During the 12 months previous, there were 64 sales with an average sales price of $2,015,577; these homes were on the market for an average of 30 days; combined days on the market is 87.

SINGLE-FAMILY BONITA BAY HOMES

- During the last 12 months, there were 48 sales with an average sales price of $2,173,766; these homes were on the market an average of 31 days; combined days on the market is 100.

- During the 12 months previous, there were 48 sales with an average sales price of $2,185,484; these homes were on the market for an average of 40 days; combined days on the market is 105.

For a list of BONITA BAY homes sold in the last 12 months, click here.

For a list of BONITA BAY homes that are pending at the moment, click here.

November 2023 Market Update

Buyers’ Tactics in the Face of High Mortgage Rate

By Holden Lewis

By Holden Lewis

Buyers may be able to make rising mortgage rates less onerous by using one or more of these nine tips suggested by RE agents and lenders.

Mortgage rates have risen to their highest levels in more than 20 years, making it harder to afford a home. And yet, out of necessity or desire, hundreds of thousands of people buy homes every month.

With the 30-year fixed rate topping 7%, NerdWallet asked real estate agents and mortgage loan officers for advice on how homebuyers can stretch their home-buying dollars in this time of high interest rates. Here are nine tactics that they suggested.

1. Ask the seller to reduce the mortgage rate

Temporary mortgage rate buydowns have become commonplace since rates surged in early 2022. With a temporary rate buydown, the seller pays a portion of the buyer’s interest payments upfront. This reduces the house payments for the first one, two or three years of ownership.

“This is a common strategy for new-home builders, but it can also be used in the purchase of resale homes,” said John Bianchi, executive vice president for loanDepot. (All sources in this story commented via email.) “Negotiating a temporary buydown with the seller can help soften the blow of high interest rates, reducing your monthly payment for one to three years.”

In one typical setup, the seller’s payment effectively cuts the buyer’s interest rate by 2 percentage points in the first year, and by 1 percentage point in the second year. After that, the buyer pays the full interest rate. This is known as a 2-1 buydown.

Another option is to reduce the mortgage rate permanently, using discount points. One discount point equals 1% of the loan amount; each point typically reduces the interest rate by around 0.25 percentage point.

“Homebuyers have an opportunity to get a seller to pay for these methods to lower their interest rate,” said Chuck Vander Stelt, a real estate agent in Valparaiso, Indiana. “Some homebuyers should seriously consider offering a more generous price to the seller in exchange for a large closing cost concession and then use those funds to buy down the interest rate as much as possible.”

2. Use part of your down payment to pay down debt

When you apply for a mortgage, the lender considers your total debt payments for the house, car, student loans and credit cards. Sometimes it makes sense to divert some of your intended down payment money to cut the higher-rate debt first, said David Kuiper, vice president and senior mortgage banker for Dart Bank in western Michigan.

“While the mortgage payment will be slightly higher, the total debt/payments is lower, making the proposed purchase more affordable,” Kuiper said.

3. Use homebuyer assistance programs

State and local governments sponsor an abundance of programs to make homes affordable for homebuyers, especially first-timers. Some programs offer down payment assistance and help with closing costs. Others offer favorable interest rates or tax credits.

Details differ from state to state. Some programs are targeted to certain counties, cities or neighborhoods. Others are intended for specific groups of people, such as teachers, first responders or renters who live in public housing. Some programs have income limits.

4. Ask the seller to finance the purchase

You can give the seller an IOU for part of the home’s value and make monthly payments directly to the seller at an interest rate that’s lower than you could get from a bank. This arrangement is called “seller financing” and has its roots in the early 1980s, when mortgage rates zoomed as high as 18%. You might wonder why a seller would agree to such a deal.

“They will often do this in order to get the price they want,” said Janie Coffey, who leads the Coffey Team with eXp Realty in St. Augustine, Florida. The seller gets full price while you get a break on the interest rate.

Seller financing usually has an end date: Within three, five or 10 years, the buyer must get a mortgage from a lender to pay off the amount owed to the seller. Coffey explained that the type of seller open to this arrangement often has paid off the mortgage “and is OK to wait for their big payoff.”

Seller financing is complex. Use an experienced real estate attorney to draw up the contract.

5. Don’t wait for a rate you like better

“If the right house comes along and the payment is affordable (even if you don’t like the interest rate), you should buy the house,” Kuiper said.

You often hear that you should buy now and refinance someday, after interest rates fall. That’s not Kuiper’s point. His point was this: If mortgage rates fall, more buyers will rush into the market. They’ll make competitive offers and drive home prices higher, “essentially wiping out any advantage of the lower interest rate.”

6. Don’t get distracted by things you don’t need

Some sellers want flexibility about the closing date, would prefer the buyer to make repairs, and are scared of accepting an offer from a buyer who ends up failing to qualify for the mortgage.

Vander Stelt advises staying focused on price with these hassle-avoidant sellers, while being flexible on the rest of the offer on the house. “Do this by offering the best terms you can, including buying the home as-is, a closing date and possession that works best for the seller, and illustrating how strong of a candidate you are to get your mortgage approved,” he said.

You can demonstrate that you’re a strong mortgage candidate by showing a preapproval letter and by sharing financial information, such as account balances that prove you have the cash for the down payment.

7. Buy a house that needs work

Buying a fixer-upper is an old-fashioned, time-tested way to save money.

“If you can be patient, it’s worth buying a home that needs work and slowly fixing it up over time or taking a renovation loan to acquire the home and do the work upfront,” said Brian Koss, regional sales director for Movement Mortgage, in Danvers, Massachusetts.

8. Build a house or buy a brand-new one

“Building a new home can provide more certainty around how long you will have to wait to move in, it can provide more cost certainty, and it can save you money in the short and long term by avoiding costly remodels, appliance repairs and unexpected repairs of older parts of the home,” said Jeffrey Ruben, president of WSFS Mortgage in the Greater Philadelphia area.

Buying a new home in a development has some of the same advantages. And today’s buyers have good reason to shop for new construction because there’s a shortage of existing homes for resale.

9. Rent out part of the house

Coffey suggested using an old strategy with a trendy name – house hacking – “buying a property like a duplex, where you live in one unit and rent out the other,” she said.

If you buy a duplex, triplex or quadplex, and you live in one unit, you can include the expected rental income for the others when qualifying for a loan. In some cases, you can qualify for a mortgage using expected rental income from an accessory dwelling unit, such as a basement apartment or a tiny house in the backyard.

If you buy a home today, you’re stuck with high mortgage rates for the time being. But by employing some creativity, you might find a way to afford homeownership.

© 2023 WBTW, Nexstar Broadcasting, Inc.

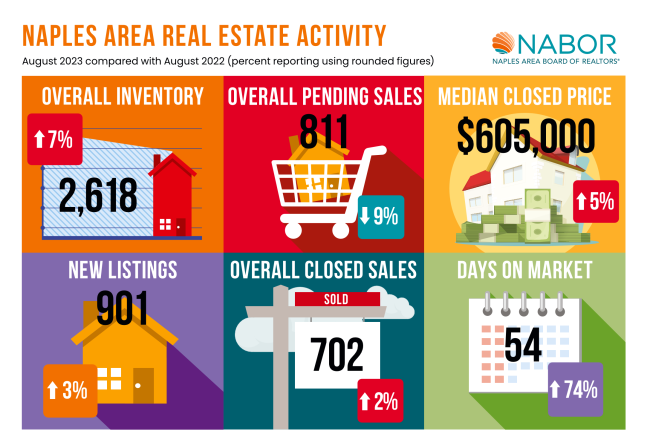

Market Resiliency Fuels Home Sales in August

Inventory is selling quickly, and prices are stable in the Naples housing market. According to the August 2023 Market Report by the Naples Area Board of REALTORS® (NABOR®), which tracks home listings and sales within Collier County (excluding Marco Island), closed sales of homes in Naples during August increased 17 percent compared to July closed sales, and 1.9 percent to 702 closed sales from 689 closed sales in August 2022. Brokers who reviewed the Market Report are confident sales during the second half of 2023 could outperform sales during the second half of 2022, unless we experience another major disaster like a hurricane. Another promising factor that supports this expectation is the steady rate of new listings, which increased 2.6 percent in August, and contributed to the 7.2 percent increase in inventory for the month.

|

|

|

|

“Even in a time of economic volatility and uncertainty, Florida still provides benefits as a tax haven compared to other states with high taxation and cost of living rates,” said Jillian Young, President, Premiere Plus Realty, who added that “sellers waiting until winter season to list their home may miss out on the buyers who want to purchase a home before the end of the year and before more anticipated rate hikes.” Young also went on to say that “if the housing market’s activity continues to perform at the same steady rate we’ve enjoyed so far this year – and current market conditions show it has the potential – then it’s likely homeowners could enjoy a 7 percent increase in home value by year end. The fact that properties didn’t lose value during a year after a major hurricane will only strengthen the desirability of future homeownership in Naples.” Broker analysts are not optimistic that inventory will rise above 3,000 properties in the next year. According to Jeff Jones, Broker at Keller Williams Naples, “The report showed 731 price decreases in August. I tell my agents that these should be considered ‘new listings’ as the new lower list price will be attractive to a set of new buyers seeking homes in that new lower price range.” If you are looking to buy or sell a home in Naples, contact a Naples REALTOR® who has the experience and knowledge to provide an accurate market comparison or negotiate a sale. A REALTOR® can ensure your next purchase or sale in the Naples area is a success. Search for your dream home and find a Naples REALTOR® on Naplesarea.com.The Naples Area Board of REALTORS® (NABOR®) is an established organization (Chartered in 1949) whose members have a positive and progressive impact on the Naples Community. NABOR® is a local board of REALTORS® and real estate professionals with a legacy of nearly 60 years serving 6,000 plus members. NABOR® is a member of the Florida Realtors and the National Association of REALTORS®, which is the largest association in the United States with more than 1.3 million members and over 1,400 local board of REALTORS® nationwide. NABOR® is structured to provide programs and services to its membership through various committees and the NABOR® Board of Directors, all of whose members are non-paid volunteers.

The term REALTOR® is a registered collective membership mark which identifies a real estate professional who is a member of the National Association of REALTORS® and who subscribe to its strict Code of Ethics.

|

|

|

|

Why Chose Me as Your REALTOR®?

To learn more about me and my real estate business and Bonita Bay real estate specifically, I encourage you read the About Ed section as well as the Testimonial section of the site. Over the years, my clients have expressed their satisfaction in my services and I’ve showcased their kind words so you can determine if I am the right REALTOR® to represent you.If you are curious as to my sales success, visit my Sold Homes page. This gives a clear picture of exactly what I’ve accomplished and, more importantly, what I can accomplish for you. |