01 Feb Shadow Wood at the Brooks Real Estate News | February 2023

As of February 1, 2023, there are 13 active listings in our area multiple listing service (MLS) in Shadow Wood. That is 3 more than last month.

For comparison, last year on February 1, there were 4 listings in Shadow Wood.

There are 4 single-family homes on the market, listed from $999,000 to $3,249,900. The average list price is $2,349,725. The average days on the market is 131 days; the average total days on the market is 131 days.

In the condo market, there are 9 active listings ranging from $599,000 to $725,000. The average list price is $650,911. The average days on the market is 41 days; the average total days on the market is 41 days.

A reminder, you have access to the most comprehensive website devoted to Shadow Wood, www.ShadowWoodRealty.com. I’ve included maps, floor plans, photos, and descriptions of each neighborhood within this desirable community.

Please contact me for all your real estate needs in Shadow Wood. With over 35 years of helping buyers and sellers in SWFL, my experience will be invaluable in this fast-moving, low-inventory market.

Your Shadow Wood REALTOR®,

Ed Gongola

Summary of Shadow Wood Home Sales

If you are considering selling your Shadow Wood home, here are some statistics that may help you decide to place your home on the market.

SHADOW WOOD CONDOs

- Within the last 12 months, there were 27 sales; the average sales price was $622,148; and, these condos were on the market an average of 14 days; combined days on the market is 69.

- During the 12 months previous, there were 31 sales; the average sales price was $441,081; and, these homes were on the market an average of 12 days; combined days on the market is 57.

SINGLE-FAMILY SHADOW WOOD HOMES

- During the last 12 months, there were 49 sales; the average sales price was $1,627,000; and, these homes were on the market an average of 11 days; combined days on the market is 72.

- During the 12 months previous, there were 48 sales; the average sales price was $1,140,803 and, these homes were on the market an average of 27 days; combined days on the market is 74.

For a list of SHADOW WOOD homes sold in the last 12 months, click here.

For a list of SHADOW WOOD homes that are pending at the moment, click here.

February 2023 Market Update

DOWNING-FRYE: LOW-PRICED PROPERTY LISTINGS CONTINUE TO PLUMMET

“We had over $139 million in pending sales volume for the month of January 2023,” said Mike Hughes, V. P. and Gen. Mgr. of Downing-Frye Realty, Inc. “This is about what we normally see for the month of January. The big change this January was that there were very few low end pending sales. From 2010 until 2020, Downing-Frye Realty, Inc. usually had an average of about 127 pending sales (for the month of January) of properties that were listed below $250,000. This year we had eleven pending sales of properties that were listed below $250,000! The big difference is the result of a very low inventory of properties below $250,000. Currently, we don’t see the listing inventory improving much on the lower end. The low priced properties are very desirable to multiple groups including first time home buyers, retirees on a fixed income and investors. Over the last several years, we have seen the listings of low- priced properties sell quickly as they are very desirable to a lot of buyers. We should note that the other price ranges performed well for the month of January. Our winter visitors have arrived!

BONITA / ESTERO: MOSTLY CASH BUYERS

The Bonita/Estero market currently remains a sellers market with strong price points averaging 11.6% higher than December of 2021 with many factors heading in the direction of favoring the buyers including the increase of days on market, the rising inventory levels and the decrease in sold properties. Buyers seem to be more selective and taking additional time to find the right property, which has reduced bidding wars and increased days on market from 19 days in December 2021 to 35 days in December 2022. Median prices, while down from the previous month, were up almost 12% from a year ago.

“The December realtor.com Monthly Traffic Report showed 13,511,504 search page views, which continues to support the desirability of our area,” said Jerry Murphy, Managing Broker of Downing- Frye’s Bonita Springs office.

NAPLES AREA: HOUSING MARKET REDEFINED

Demand for the Naples lifestyle remained constant in 2022, and low inventory pressed median closed prices upward. The overall median closed price in December 2022 increased 13.9% to $575,000 from $505,000 in December 2021. New home builds slumped in December, and new construction sales consumed 16.7% of all closed sales in December, up slightly compared to the previous two months. Demand for homes in 2022 kept REALTORS® busy looking for new listings, which dropped 8.4% to 13,577 compared to 14,819 in 2021. Only 105 homes were for sale below $300,000 in December compared to 1,816 in December 2019. Mike Hughes, remarked that “aside from the below $300,000 price category, inventory nearly doubled in every other price category by the end of 2022 compared to 2021.”

MARCO ISLAND AREA: 2022 ACTIVITY REPORTED

The Marco Island Area Assoc. of Realtors® reported year-end figures for 2022: 327 homes were sold for the median sell price of $1.8M (up 44% from 2021) averaging 44 days on the market; 495 condos were sold for the median sell price of $680K (up 24% from 2021) averaging 38 days on the market; 117 lots were sold with the median sell price of $835K averaging 109 days on the market. The total inventory at the end of 2022 was 281 properties (up 4% from 2021).

FLORIDA: BALANCE RETURNING

At the end of 2022, statewide closed sales of existing single-family homes totaled 287,352, down 18% compared to the 2021 year-end level; and for condo-townhouses, a total of 125,494 units sold statewide in 2022, down 21.7% compared to 2021. “The good news is, we have a lot more inventory than what we had over the pandemic years,” Florida Realtors® Chief Economist Dr. Brad O’Connor said. “Active listings of single-family existing homes more than doubled from a 1-month supply at the end of 2021 to a 2.7-months’ supply at the end of 2022. If we get a little relief in mortgage rates, then all the other factors are still there that make Florida appealing and a strong draw for buyer demand.”

USA: PENDING SALES INCREASE

Pending home sales increased in December for the first time since May 2022 — following six consecutive months of declines. “This recent low point in home sales activity is likely over,” said NAR Chief Economist Lawrence Yun. “Mortgage rates are the dominant factor driving home sales, and recent declines in rates are clearly helping to stabilize the market.”

Sources: The Bonita Springs-Estero REALTORS®/SWFLMLS, Naples Area Board of REALTORS®, National Assoc. of REALTORS®, Florida REALTORS® and Marco Island Area Assoc. of REALTORS®

Are Floridians More Optimistic than Rest of U.S.?

By Kerry Smith

While Americans’ attitudes declined a bit in Jan., a monthly UF study of Floridians found a 1.4-point increase overall with an uptick in expectations for the future.

In January, consumer sentiment among Floridians increased 1.4 points to 65.4 from December’s revised figure of 64. At a national level, sentiment increased over five points. Yesterday, the Conference Board noted a slight dip in overall Americans’ optimism.

“The increase in consumer sentiment in January stems from improvements in Floridians’ expectations about the future, particularly their expectations of a year from now,” says Hector Sandoval, director of the Economic Analysis Program at UF’s Bureau of Economic and Business Research.

Sandoval calls those views “consistent with a falling inflation outlook. After peaking at 9.1% in June, inflation has steadily declined to 6.5% in December. It is expected that price pressures will continue to ease over the next few months, preventing households from experiencing further hardships.

Among the five components that make up the index, four increased and one decreased.

Current conditions: Floridians’ opinions about current economic conditions in January were mixed. Views of personal financial situations now compared with a year ago increased 1.1 point from 54.6 to 55.7. On the other hand, opinions as to whether it’s a good time to buy a major household item like an appliance decreased three-tenths of a point from 55.2 to 54.9.

Future conditions: Outlooks about expected future economic conditions were positive.

Prospects for individual’s personal finances a year from now increased 3.3 points from 76.5 to 79.8. Similarly, expectations about U.S. economic conditions over the next year increased 1.6 points from 62.9 to 64.5.

This long-range optimism even extended five years into the future. Views of U.S. economic conditions over the next five years increased 1.1 points from 70.9 to 72.

Meanwhile, the Florida labor market continued to strengthen in December, with more jobs being added. According to the latest Florida jobs report, the unemployment rate ticked down by 0.1 percentage point in December, reaching 2.5% – only one-tenth of a percentage point above the lowest rate on record.

In line with this, the number of Florida workers seeking unemployment benefits is hovering around pre-pandemic levels, indicating a tightening labor market.

“Prices have been declining over the second half of 2022 as the Fed swiftly increased interest rates,” says Sandoval. “Despite this, the U.S. economy grew at an annual rate of 2.9% in the last quarter of 2022.”

Inflation, however, remains well above the Federal Reserve target of 2%.” While the Fed will likely raise rates this week, it’s not expected to be a large increase similar to last year.

Still, “continued increases in interest rates will ultimately slow down the economy and trigger a recession,” adds Sandoval.

Sandoval remains positive, though, “Looking ahead, with the assumption the labor market remains robust, we expect consumer sentiment to improve slowly as inflation pressures continue to ease.”

The index used by UF researchers is benchmarked to 1966, which means a value of 100 represents the same level of confidence for that year. The lowest index possible is a 2, the highest is 150.

© 2023 Florida Realtors®

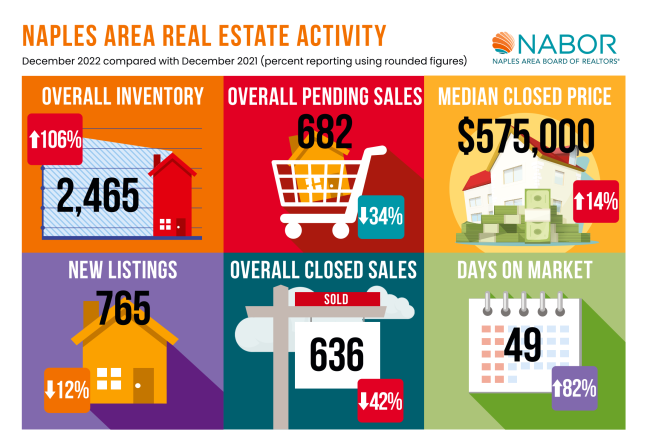

Naples Housing Market Redefined

In the first year after a two-year interruption in normal activity caused by the COVID-19 pandemic, the Naples real estate market is stable in terms of value, but there are not as many homes to choose from, and prices have elevated. As pandemic restrictions loosened in 2022, sellers and buyers pivoted their attention from the housing market to the travel market. As a result, and according to the December 2022 and 2022 Annual Market Report by the Naples Area Board of REALTORS® (NABOR®), which tracks home listings and sales within Collier County (excluding Marco Island), overall closed sales in 2022 decreased 34.8 percent to 10,156 properties from 15,570 properties in 2021. And while inventory is beginning to rebound, increasing 106.3 percent to 2,465 properties in December 2022 from 1,195 properties in December 2021, broker analysts reviewing the report are uncertain where and when an influx of inventory will arrive to meet our pre-pandemic levels.

|

|

| If you are looking to buy or sell a home in Naples, contact a Naples REALTOR® who has the experience and knowledge to provide an accurate market comparison or negotiate a sale. A REALTOR® can ensure your next purchase or sale in the Naples area is a success. Search for your dream home and find a Naples REALTOR® on Naplesarea.com. The Naples Area Board of REALTORS® (NABOR®) is an established organization (Chartered in 1949) whose members have a positive and progressive impact on the Naples Community. NABOR® is a local board of REALTORS® and real estate professionals with a legacy of nearly 60 years serving 6,000 plus members. NABOR® is a member of the Florida Realtors and the National Association of REALTORS®, which is the largest association in the United States with more than 1.3 million members and over 1,400 local board of REALTORS® nationwide. NABOR® is structured to provide programs and services to its membership through various committees and the NABOR® Board of Directors, all of whose members are non-paid volunteers. The term REALTOR® is a registered collective membership mark which identifies a real estate professional who is a member of the National Association of REALTORS® and who subscribe to its strict Code of Ethics. |

The Rent Problem: Where Fla. Stands Now |

TaxWatch: Fla. is almost a victim of its own success. New renters poured into the state, notably during the pandemic, but found too few homes to accommodate them.

INVERNESS, Fla. – Florida aims to be the best state in the nation to live, work, and play, and its tremendous growth suggests such efforts have not been in vain. Florida welcomes about 808 new residents per day, and for the first time since 1957, the state has the fastest-growing population within the United States. While tough to manage at times, a growing population is good for the state, fueling Florida’s economy with new talents and dollars. But as the state continues to attract new residents, the state must ensure that the development of housing keeps pace.

Following the COVID-19 pandemic, Florida experienced a housing boom. As discussed in the October 2021 Florida TaxWatch commentary “Beyond the Pandemic: Long-term Changes and Challenges for Housing in Florida,” a collision of demographic trends, government policies, and basic supply and demand resulted in soaring house prices. By November 2022, the median price of single-family homes in Florida was nearly 10% higher than the year before.

The high prices of houses make homeownership seem out of reach to would-be homebuyers, which can lead to these households choosing to be renters. This places an extra strain upon the rental market, causing price spikes. The increase of rental prices burdens the budgets of Floridians – whose budgets are already burdened by inflated prices on goods – and results in long-lasting implications for Florida’s workforce.

Nationwide, the prices of rent have drastically grown since the days before the COVID-19 pandemic. Florida incurred a 36% increase in rental prices from the first month of 2020 to the last month of 2022. Florida’s rental prices grew especially fast in 2021. At the start of the year, the median price of rent was $1,266. By the year’s end, renters were paying $1,635, a 29% increase.

The speed of growth slowed after 2021, and prices even experienced decreases during the last four months of 2022. Although slight declines in rental prices are common during the end of the year, the national rate of decline coupled with increased vacancy rates may be promising.

Preliminary forecasts suggest that relaxing rental demand and increased supply should continue easing price growth in coming months; however, since the price is not expected to decline, renters will continue to grapple with the legacy of the 2021 price hike. Rent in metropolitan areas like Miami, Tampa and Fort Myers has drastically increased since 2020.

Metropolitan areas are popular for renters looking for job opportunities, and amid the rise of remote work, many of these cities have also become popular with employed persons looking for an enjoyable place to live. Households in Miami pay a median of $1,634 for a one-bedroom apartment and a median of $2,079 for a two-bedroom apartment, both of which cost about 36% more than the median prices of January 2020.

Rental prices have grown so much that they surpassed the prices predicted by historical trends. According to the Waller, Weeks and Johnson Rental Index, a rental market is considered “overvalued” when it exceeds projections. Of the 25 most overvalued rental markets nationwide, with costs ranging from 7.06% to 18.05% higher than predictions, Florida is home to nine: Cape Coral (ranked #1), Miami (#2), North Port (#3), Tampa (#7), Orlando (#12), Deltona (#14), Palm Bay (#16), Jacksonville (#18), and Lakeland (#21).

High rent is a risk to Florida’s workforce. While Florida’s highest earners may be able to afford committing greater funds to their housing needs, Floridians with a smaller net income may be required to compromise other needs, such as health care or insurance, to make ends meet. Some may choose to live farther from their workplace to seek affordable housing, committing to longer commute times and greater gas prices. Others may leave local communities, or even the state altogether, taking their potential earnings and talents elsewhere.

Losing residents to other states could limit the strength of Florida’s economy. Currently, the labor market is competitive, characterized by record high quit rates and changing workplace values (i.e., remote work). If Floridians leave their jobs and move to other states, it will further restrain an already tight talent pool.

Although other states are enduring high rental growth as well, there are enticing options that could draw away Floridians. Median rent in nearby Georgia ($1,390 per month) is about $300 less than Florida’s median rent ($1,698). In Texas – a state whose size, economy, and policies are similar to Florida – median rent is $400 less ($1,298).

To attract and retain the talent Florida’s economy depends upon, Florida needs sufficient housing options.

Rent is often considered affordable when it costs 30% or less of a household’s income. If gross rent costs more than 30% of a household’s income, the household is considered cost burdened, and if the household pays more than 50% of their income for rent, it is considered severely cost burdened. Lower earning Floridians are especially susceptible to becoming cost burdened. Average median income (AMI) for Florida households is about $61,777.13 Most households earning the AMI or less are cost burdened, paying 40% or more of their household income on rent.

The varied use of housing units is heavily intertwined with Florida’s success. Both as homes to the workforce and as passive sources of income, such as vacation homes or rentals, the state’s economy depends upon a reliable housing supply. With the prevalence of remote work, the state will also need enough housing units to welcome new residents who choose to bring their earnings from across the nation into Florida.

Entering the 2023 session, the Florida Legislature will tackle the challenge of determining how to best assist home and rental seekers, whether with support for making attainable housing affordable or accelerating and incentivizing construction to ensure the state can continue accommodating for the growing demand upon its housing units.

Florida TaxWatch is an independent, nonpartisan, nonprofit taxpayer research institute & government watchdog. Florida TaxWatch works to improve the productivity and accountability of Florida government. Its research recommends productivity enhancements and explains the statewide impact of fiscal and economic policies and practices on residents and businesses.

© Copyright 2023 Citrus County Chronicle, Landmark Community Newspapers LLC (LCNI). All rights reserved.

|

|

|

|

|

|

|

|

|

|